Cheap Rate Term Insurance - When to Invest

It does not seem long back when I would just sometimes encounter an ad for low-cost term life insurance. But more just recently these encounters seem to happen throughout almost any hour of a radio or television program. Unlike permanent (cash value) life insurance that is normally creatively sold or planned for, term insurance has actually become a product that customers usually acquire by themselves, without planning support. This column will certainly analyze term insurance and determine when its purchase is most suitable. I will certainly not clutter this piece with perhaps more imaginative planning alternatives or cover intrinsic prospective issues related to tax and other matters since this column is for customers of life insurance who wish to move from the desire for protection to acquiring it.

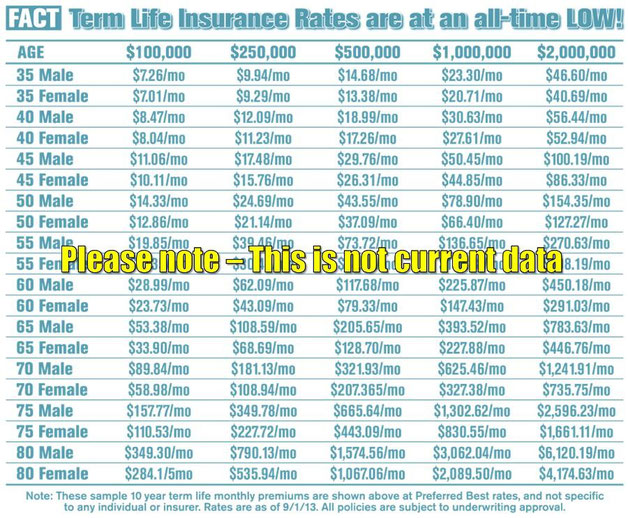

Low Cost

Very low term insurance costs are accomplished by separating prospective insureds into 3 classifications: super-perferred, preferred, and requirement. Generally, a super-preferred rating is earned by not using tobacco and having excellent to excellent height/weight ratios, blood values, health history, individual practices, and family health history. A lower preferred rating is earned when a couple of of the locations needed for super-preferred are a bit weaker. Requirement is offered to insureds who have greater weaknesses in any of the essential underwriting locations. Provided the exceptional health of super-preferreds and the restricted protection duration, these policies are comparable to unexpected death insurance coverage.

You should understand that some aggressive online marketers of affordable term insurance will advertise or estimate term costs based upon their super-preferred score category despite the real health of a certain possible insured. This possible dichotomy in between the quoted super-preferred cost and the real cost after the underwriting process has been completed has actually triggered some customers to feel like they have actually been victims of a mindful bait-and-switch strategy because a preferred score is usually one-third higher in cost than super-preferred, while standard is twice the expense.

Duration and Conditions

5-, 10-, 15- and 20-year level term policies are the most typical. The level term classification implies the expense remains constant for the duration of time designated. Numerous level term policies' premiums are ensured for the specified period of time. Numerous can be renewed after the specific amount of time with evidence of ongoing health or the expense to continue protection can be extremely high. The renewal cost will not be understood ahead of time since business change them at their discretion. Numerous policies can be converted, without additional proof of health, to irreversible policies the business so designates.

Likewise readily available are annual renewal term [ART] policies, whose expenses go up incrementally each year. ART is suitable when the protection is just needed for less than 5 years. For example, a creditor might require insurance protection on a credit line to a small company for a short time period. ART would likewise be the much better choice if the insured means to convert to irreversible coverage within 5 years when his cash flow improves.

Term life insurance is the suitable insurance coverage approach for these scenarios:

Family Protection

The primary purpose for life insurance is to offer defense to those financially depending on you. Let's think about Matt Green, a recently licensed internist taking his first post-training task. Matt's wife does not work outside the home, and they have 2 little ones. His yearly wage is $100,000. Without much calculation, he identifies he wants to protect his family with $2.0 million worth of life insurance. He isn't really thinking about considering any expensive life insurance or tax planning, so he contacts one of the companies marketing inexpensive term insurance, complies with their underwriting requirements, gets a super-preferred rating. He acquires a 10-year level term policy for $2.0 million at an annual expense of $630, which is less than the device expense for group policies through such expert companies as the American Medical Association. Matt's mindset is: With little expense in time or cash, he can now forget abou t his life insurance requires for 10 years.

Fund Buy-Sell Agreements

Business owners frequently have arrangements that obligate either each other or business entity to acquire a departed partner's interest in business (See the April and August 1997 AAII Journal Insurance Products columns that went over buy-sell arrangements and life insurance). Such commitments should be moneyed with life insurance. For business owners who have limited cash circulation or intend on selling or liquidating the company within a specific period, term insurance is a good alternative.

Estate Liquidity

Usually, estate liquidity life insurance is held up until the death of the guaranteed(s), so term insurance isn't really naturally cost efficient. That is, when the life insurance will certainly be held up until death and the guaranteed lives to life span or beyond, term insurance will certainly probably become too costly. Nevertheless, in cases where estate owners have extremely illiquid possessions that are most likely to be sold or liquidated within a provided time period and personal capital is a problem, using term insurance as a short-lived liquidity fund is an excellent idea. As soon as the illiquid possessions have been sold or liquidated, the estate owner then might think about transforming the term insurance to an irreversible kind of life insurance, possibly as a wealth transfer asset.

Policy Replacements

The cost, primarily for the level term policies, has actually been on a downward trend (occasionally approaching a spiral) for the previous decade. Since of this, lots of purchasers of level term policies have actually changed their policies before the level term duration ends. Comparing costs is simple. Nevertheless, there are two intangibles to think about before going on with the policy replacement. First, for the replacement policy, there is a new two-year period during which if death happens the insurance business will certainly examine to determine whether there were any misrepresentations on the insurance coverage application. If they can prove there were, they will attempt to reject the claim. Likewise, if death is by suicide, no benefits are paid during the very first 2 years. Second, consider the quality of the company and expense of transforming to a long-term policy. Typically, the quality of the business isn't really as much of a concern with guaranteed-cost term insurance, but it is with long-term insurance coverage. And, converting to a full-load irreversible policy is less bring in ive than being able to convert to a low-load permanent policy.

Premium Guarantees

I am not familiar with any term policies' guaranteed premiums being changed or death benefits not being paid, a minimum of during this century. However level term insurance is so competitive, with lower and lower rates coming out, that it wouldn't amaze me if some business wind up being taken by regulators due to solvency concerns. If that were to occur, we would remain in uncharted waters regarding the effects it would have on policy owners. My suggestions is that, besides expense, you should consider the quality of the business, and particularly the amount of inexpensive term insurance the business offers as a percentage of its other life insurance business.

Purchasing Term Insurance

Previously this year, Ameritas Life Insurance Corporation, through its low-load direct-to-consumer-unit Veritas (800/552 -3553), began marketing and selling 10- and 20-year level term insurance with some of the most affordable premium costs readily available.

As an option to Ameritas, you can call Insurance Information (800/472 -5800) and for a $50 cost they will provide you the names of insurance business (consisting of Ameritas) with the most affordable rates based upon your specific circumstance.